![]()

November 16, 2017 by Hamilton Capital

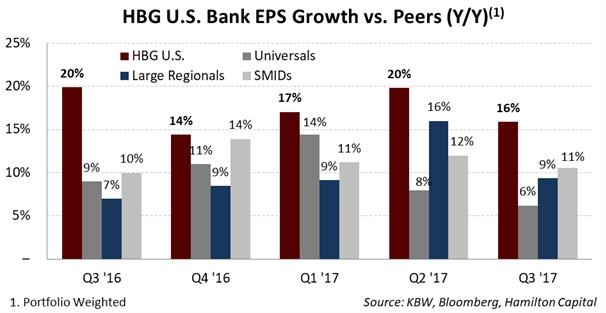

In the Hamilton Capital Global Bank ETF (Ticker: HBG), the U.S. bank portfolio reported another very strong quarter, posting portfolio-weighted earnings growth of ~16% Y/Y, its fifth consecutive quarter of double-digit Y/Y growth.

HBG is up 10.3% YTD (through October 31st), making it 13% ahead of the KBW Global Bank Index (CAD). HBG continues to generate very consistent performance, with comparatively low drawdowns versus global bank indices, and U.S. banks, in particular. For example, the ETF has experienced only 5 negative months, versus 8 for the Canadian banks and 9 for the U.S. banks.

HBG’s return also compares very favourably with other developed market global bank indices, including the U.S., Japan, and Australia, and is in line with the U.K. and Canadian banks, but lower than the European banks. Emerging market banks have performed very well YTD, with Chinese banks – which HBG does not hold – rising 15% in CAD.

Of note, the U.S. banks – which account for over 40% of HBG’s portfolio – have had a very difficult year as a group, with the regional banks performing the worst (over this period, the KRE was down 0.4% in CAD and up 3.9% in USD). Although U.S. mid-cap banks represent (by far) the largest percentage of HBG, it was still up over 10% YTD. One of the reasons for HBG’s strong performance despite U.S. banks large allocation and underperformance is the superior EPS growth of the ETF’s U.S. bank holdings supported by their “high teens” average EPS growth.

This is the fifth consecutive quarter where HBG’s U.S. mid-cap bank portfolio experienced higher EPS growth than the mid-caps, the universals, and the large regionals as highlighted by the chart below.

As we have noted in the past, with ~180 U.S. mid-cap banks (i.e., those with market caps between $0.5 bln and $20 bln), there is greater opportunity to construct a portfolio with superior earnings potential and more targeted attributes including higher rate sensitivity, M&A potential, higher loan growth and valuation support.

Despite their weak stock performance year-to-date, U.S. banks continued to post improving operating trends in Q3-17. Of the 215 reporting institutions covered by Keefe, Bruyette and Woods (KBW):

- Profitability: Median earnings growth was 10% y/y; median ROE was 9.2%, or ~30 bps higher Y/Y

- Note, HBG’s U.S. bank earnings growth was 16% Y/Y, portfolio-weighted

- Revenues: Net interest income drove the rise in revenues, with median growth of 11% Y/Y, supported by expanding net interest margins and strong loan growth:

- The median NIM was 3.52%, up 8 bps Y/Y

- Average loan balances showed strong growth at +10% Y/Y (with over 90% of reporting institutions showing positive loan growth Y/Y)

- Efficiency: Revenues continue to outpace expenses, with the median efficiency ratio now below 60% (59.5%, down 185 bps Y/Y)

- Credit quality: Credit continued to improve, with non-performing assets falling to 0.65% of average loans (down 17 bps Y/Y), and provisions for credit losses declining further (down 2 bps to just 14 bps), while net charge-offs remained very low at 9 bps (unchanged Y/Y)

- Capital: Capital levels remained robust: the median TCE ratio (tangible common equity to tangible assets) rose 9 bps Y/Y to 9.2%

Note: Comments, charts and opinions offered in this commentary are produced by Hamilton Capital and are for information purposes only. They should not be considered as advice to purchase or to sell mentioned securities. Any information offered is believed to be accurate, but is not guaranteed.