For HDIV and HYLD, we aim to create higher income ETF versions of the S&P/TSX 60 and S&P 500, respectively. Investors in HYLD will recall we recently swapped HBF for JEPI (see HYLD – Adding JEPI, Selling HBF for Higher Yield, Added Diversification, Lower Fees for additional information). Today’s insight discusses our next meaningful adjustment to HYLD’s portfolio, and why we believe it will help better achieve its investment objective of providing attractive monthly income and the opportunity for long-term capital appreciation.

Adding JPMorgan Nasdaq Equity Premium Income ETF (JEPQ); Selling CI Tech Giants Covered Call ETF (TXF)

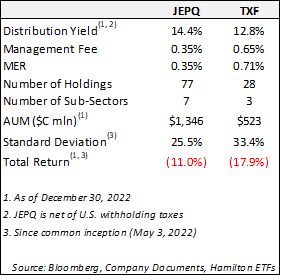

As part of HYLD’s ongoing review, we have recently added JPMorgan Nasdaq Equity Premium Income ETF (JEPQ) and sold the CI Tech Giants Covered Call ETF (TXF). In our opinion, JEPQ offers several advantages over TXF, as highlighted in the table below. Specifically, JEPQ has: (i) a higher distribution yield (14.4% net of U.S. withholding taxes vs. 12.8% for TXF, as of December 30th); (ii) a significantly lower management expense ratio or MER (0.35%, or less than half of TXF’s 0.71%[1]); (iii) greater diversification (both by position and sector); and (iv) lower volatility (since JEPQ’s launch in May 2022)[2]. Finally, the addition of JEPQ also helps align HYLD’s sector mix more closely to that of the S&P 500, which should increase its correlation to the index.

Since it was launched in May 2022, JEPQ has outperformed TXF by 6.9%[3]. Notwithstanding the fact that past performance is not indicative of future performance, we believe this switch supports the longer-term objectives of HYLD, including providing a higher yield.

HYLD: Stronger Underlying Distributions, Reduction in Fees, Greater Diversification

In our view, this change strengthens the Hamilton Enhanced U.S. Covered Call ETF (HYLD), by increasing its underlying distribution yield, providing greater diversification by holdings and by sector. Also, of note, JEPQ has a management expense ratio of less than half of TXF, which should reduce the weighted average management expense ratio of HYLD going forward. And, as noted, this change will more closely align HYLD’s sector mix with the S&P 500, which could increase its correlation to this benchmark.

HYLD is offered in Canadian and U.S. dollar versions (HYLD is CAD hedged, while HYLD.U is USD unhedged). Investors seeking to ensure their monthly distributions are not impacted by changes in the Canadian dollar are likely to prefer HYLD. Investors that seek direct U.S. exposure including currency are likely to prefer HYLD.U. The current yield of Hamilton Enhanced U.S. Covered Call ETF (HYLD) is 14.25%, paid monthly[4].

We would also note, HYLD has a sister ETF, the Hamilton Enhanced Multi-Sector Covered Call ETF (HDIV), which is designed for investors seeking a higher yielding ETF focused on the Canadian equity markets. Since its launch, HDIV has outperformed the S&P/TSX 60 index by nearly 7% as of year-end (and since inception annualized outperformance of ~4.6%)[5]. Notwithstanding the modest leverage of HDIV, in 2022 – a large down year – it outperformed this benchmark by 3.7%.

It is our view that the sector mixes of the Canadian and U.S. equity markets are highly complementary, and therefore, we believe HDIV and HYLD held together can be core holdings for investors seeking higher income versions of the Canadian and U.S. equity indices.

____

A word on trading liquidity for ETFs …

Hamilton ETFs are highly liquid ETFs that can be purchased and sold easily. ETFs are as liquid as their underlying holdings and the underlying holdings trade millions of shares each day.

How does that work? When ETF investors are buying (or selling) in the market, they may transact with another ETF investor or a market maker for the ETF. At all times, even if daily volume appears low, there is a market maker – typically a large bank-owned investment dealer – willing to fill the other side of the ETF order (at the bid/ask spread).

Commissions, management fees and expenses all may be associated with an investment in the ETFs. The relevant prospectus contains important detailed information about each ETF. Please read the relevant prospectus before investing. The ETFs are not guaranteed, their values change frequently and past performance may not be repeated.

Certain statements contained in this insight constitute forward-looking information within the meaning of Canadian securities laws. Forward-looking information may relate to a future outlook and anticipated distributions, events or results and may include statements regarding future financial performance. In some cases, forward-looking information can be identified by terms such as “may”, “will”, “should”, “expect”, “anticipate”, “believe”, “intend” or other similar expressions concerning matters that are not historical facts. Actual results may vary from such forward-looking information. Hamilton ETFs undertakes no obligation to update publicly or otherwise revise any forward-looking statement whether as a result of new information, future events or other such factors which affect this information, except as required by law.

[1] As of June 30, 2022

[2] Volatility as measured by the annualized standard deviation of returns.

[3] As of December 30, 2022

[4] As of December 30, 2022

[5] HDIV was launched on July 19, 2021. Source: Hamilton ETFs, Bloomberg