In Q2 2019, portfolio-weighted EPS[1] grew 12% for the holdings in the Hamilton U.S. Mid-Cap Financials ETF (USD) (ticker: HFMU.U). The growth in the quarter was nearly 200 bps ahead of the large cap financials at 10.1%[2] and has outgrown its large cap peers every quarter since HFMU.U was launched eight quarters ago.

Note to Reader: This Insight includes references to certain Hamilton ETFs that were active at the time of writing. On June 29, 2020, the following mergers took place: (i) Hamilton Global Financials Yield ETF and Hamilton Global Bank ETF into the Hamilton Global Financials ETF (HFG), (ii) Hamilton Australian Financials Yield ETF into the Hamilton Australian Bank Equal-Weight Index ETF (HBA); (iii) Hamilton Canadian Bank Variable-Weight ETF into the Hamilton Canadian Bank Mean Reversion Index ETF (HCA), and (iv) Hamilton U.S. Mid-Cap Financials ETF (USD) into the Hamilton U.S. Mid/Small-Cap Financials ETF (HUM).

The strong earnings growth was driven by steady volume growth, a benign credit environment, and aided by an emphasis on higher growth U.S. states and MSAs. While margins came under pressure amid lower asset yields, they are broadly expected to stabilize as funding costs moderate with lower policy rates. For a majority of portfolio holdings, earnings were a beat to consensus expectations.

Within HFMU.U, the U.S. mid-cap bank holdings were key earnings growth drivers (~60% weight) and as in past quarters earnings for this sub-sector grew by double-digits. The U.S. mid-cap banks 13% y/y EPS growth was more than 800 bps higher than the regional/trust banks. HFMU.U’s wealth management and insurance positions grew EPS by 9% and 12% y/y respectively (versus 4% growth and 12% growth for large-cap wealth managers and insurers respectively).

This is the eighth consecutive quarter since the ETF’s inception that earnings growth for HFMU.U’s holdings has outpaced the U.S. large-cap financials and in most quarters, this difference has been material. As the chart below highlights, portfolio-weighted EPS growth for HFMU.U has been in the mid-to-high teens for nearly every quarter since inception (excluding the benefit of the U.S. tax reduction – which added an additional ~18%-20% to EPS growth during 2018).

We attribute HFMU’s meaningfully higher EPS growth to stock selection with an emphasis on: (i) U.S. MSA/states with higher population and economic growth, (ii) overweighting mid-cap banks and wealth managers with steady interest rate sensitivity (in a period of more dovish Fed Funds rate expectations), and less significantly (iii) ongoing industry consolidation. Against the backdrop of a still robust U.S. economic expansion and healthy industry fundamentals, we believe consolidation is poised to accelerate across all financial sub-sectors, including banking – a view supported in part by the BBT-STI transaction earlier this year (see our February 8th, 2019 insight, “U.S. Bank M&A: Implications from the Largest Deal in a Decade”).

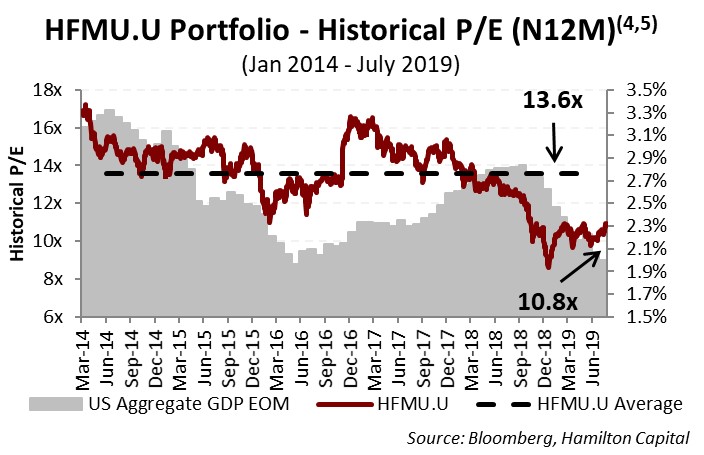

We continue to believe that investors seeking exposure to the U.S. financials sector should allocate a material component to U.S. mid-caps given the category’s significant breadth and strong operating fundamentals as well as a more favourable regulatory backdrop. Moreover, U.S. mid-cap financials continue to trade at valuation discounts to their long-term average, offering the potential for multiple expansion. As the chart below highlights, the current holdings of HFMU.U trade at 10.8x, a 21% discount to their five-year average.

____

A word on trading liquidity for ETFs …

HFMU.U is a highly liquid ETF that can be purchased and sold easily. ETFs are as liquid as their underlying holdings and the underlying holdings in HFMU.U trade millions of shares each day.

How does that work? When ETF investors are buying (or selling) in the market, they may transact with another ETF investor or a market maker for the ETF. At all times, even if daily volume appears low, there is a market maker – typically a large bank-owned investment dealer – willing to fill the other side of the ETF order (at net asset value plus a spread). The market maker then subscribes to create or redeem units in the ETF from the ETF manager (e.g., Hamilton ETFs), who purchases or sells the underlying holdings for the ETF.

Notes

[1] 100% of HFMU holdings had reported as of August 9, 2019.

[2] The U.S. financials are those represented by the S&P Financials Selector Sector Index, the S5FINL Index (ex-Berkshire). We exclude Berkshire Hathaway because its large quarterly investment gain/loss creates significant variability that disproportionately impacts the earnings growth of S5FINL (both positively and negatively). Earnings growth for each position is calculated using most recent quarterly adjusted EPS (or FFO) divided by the prior year’s quarterly adjusted EPS (or FFO), capped at +/- 100%.

[3] Portfolio-weighted average.

[4] Portfolio weights as of July 31, 2019.

[5] GDP data is a blended forward 12 month forecast of quarterly estimates. Data prior to October 31, 2014 uses actual GDP growth (versus market forecast).