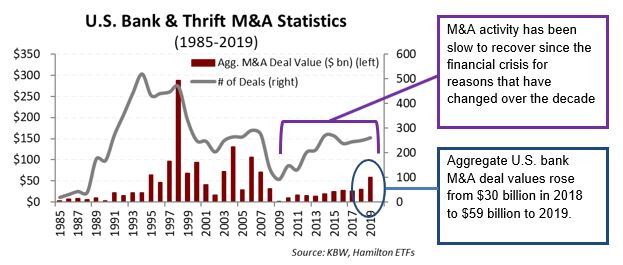

In the 10+ years since the global financial crisis, deal values in U.S. bank M&A have been slow to reach pre-crisis levels. This is notable since in the nearly 25 years preceding the financial crisis bank M&A was an important theme (particularly between 1995 to 2007) as the chart below highlights.

Note to Reader: This Insight includes references to certain Hamilton ETFs that were active at the time of writing. On June 29, 2020, the following mergers took place: (i) Hamilton Global Financials Yield ETF and Hamilton Global Bank ETF into the Hamilton Global Financials ETF (HFG), (ii) Hamilton Australian Financials Yield ETF into the Hamilton Australian Bank Equal-Weight Index ETF (HBA); (iii) Hamilton Canadian Bank Variable-Weight ETF into the Hamilton Canadian Bank Mean Reversion Index ETF (HCA), and (iv) Hamilton U.S. Mid-Cap Financials ETF (USD) into the Hamilton U.S. Mid/Small-Cap Financials ETF (HUM).

However, in 2019, we saw the first meaningful pick-up, with deal values rising to $59 bln from $30 bln a year earlier.

Post-crisis deal values depressed for a variety of reasons, but the recent uptick is likely to rise further

The reasons for the sluggish M&A activity with the U.S. bank sector – which remains highly fragmented with over 5,000 banks – have changed over the past decade:

- Initially post-crisis, the regulators were intensely focused on building capital in the entire banking system, making capital deployment/acquisitions difficult.

- In the middle of the past decade, deal values remained low, as potential targets were reluctant to sell with earnings depressed from a hostile rate environment (and at lower multiples).

- More recently, an improved earnings environment – supported by a tightening fed cycle – produced double-digit EPS growth and reduced the incentive to sell. The U.S. bank holdings in the Hamilton Global Bank ETF (ticker: HBG) and Hamilton U.S. Mid-Cap Financials ETF (USD) (ticker: HFMU.U) have generated double-digit EPS growth every quarter for over two years.

Today, we believe U.S. bank deal values are likely to continue rising for several reasons:

- The BBT/STI transaction (which accounted for virtually all of the Y/Y increase in 2019) underscores the regulators are now open to large regional consolidation, increasing the potential for further such activity.

- EPS growth is normalizing (slowing). This should place greater emphasis on expense management as a driver of EPS growth, which favours consolidation.

- Investors shown a preference for mergers-of-equals (“MOEs”), providing management teams with a deal structure likely to be met with a favourable market reaction (for all parties). Investors favour MOE transactions since they result in a sharing of economic benefits and lower deal risk (and often double-digit EPS accretions). In 2019, there were three large MOEs last year: BBT/STI, FHN/IBKC, and TCF/CHFC[1].

Expect Canadian banks to follow trends

We expect rising M&A activity (likely with smaller premiums), particularly as the pressure to generate earnings growth in a low rate environment causes banks to focus more on expenses. Not surprisingly, since the Canadian banks have spent over US$30 bln since 2004 building their U.S. commercial banking platforms, trends in U.S. bank M&A are very important.

Should acquisition activity accelerate – particularly among the regional banks – it is likely the Canadian banks will participate to preserve their competitive positions (see our January 24, 2020 Insight, “When/Where the Canadian Banks Spent US$32 bln on U.S. Banks”).

Notes

[All values in U.S. dollars unless otherwise noted]

[1] First Horizon (FHN), Iberiabank (IBKC) and Chemical Financial (CHFC) were all holdings of Hamilton ETFs at the time of the deal announcement(s).

Related Insights

U.S. Bank M&A: Another Accretive MOE, Another Positive Market Reaction (November 6, 2019)

What U.S. Investment Bankers and Banks are Saying about M&A (September 23, 2019)

U.S. Bank M&A: 8 Drivers as Described by Rodgin Cohen (May 29, 2019)

A word on trading liquidity for ETFs …

Hamilton ETFs are highly liquid ETFs that can be purchased and sold easily. ETFs are as liquid as their underlying holdings and the underlying holdings trade millions of shares each day.

How does that work? When ETF investors are buying (or selling) in the market, they may transact with another ETF investor or a market maker for the ETF. At all times, even if daily volume appears low, there is a market maker – typically a large bank-owned investment dealer – willing to fill the other side of the ETF order (at net asset value plus a spread). The market maker then subscribes to create or redeem units in the ETF from the ETF manager (e.g., Hamilton ETFs), who purchases or sells the underlying holdings for the ETF.